.png)

Somewhere in your home's history — maybe a kitchen remodel three years ago, a new roof in 2019, an HVAC replacement when the old one finally died — there's a contractor invoice you meant to keep. You might even remember paying it. But if you can't prove it to the IRS, it never happened.

That's not a technicality. It's a tax bill. And for a growing number of American homeowners, it's a significant one.

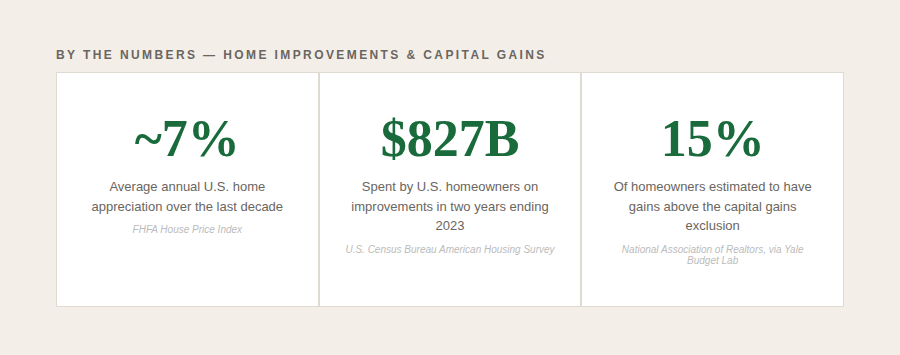

Home values have nearly doubled over the past decade. The average U.S. home appreciated roughly 7% per year over the last ten years, and in major metros, gains have been far steeper. More homeowners than ever are selling for enough profit that the federal capital gains exclusion — $250,000 for a single filer, $500,000 for a married couple — no longer covers everything. What's left over is taxable. And every improvement you can't document is ground you're giving away.

(Source: FHFA House Price Index via LendEDU; U.S. Census Bureau American Housing Survey via NerdWallet; National Association of Realtors via Yale Budget Lab)

$827B — Spent by U.S. homeowners on home improvements in two years ending 2023 (U.S. Census Bureau American Housing Survey)

15% — Estimated share of homeowners now with gains above the capital gains exclusion (NAR, cited by Yale Budget Lab)

What "Cost Basis" Actually Means — And Why It's Everything

Your cost basis is the number the IRS uses to calculate how much profit you made on your home. It starts with your purchase price — and it goes up with every qualifying capital improvement you make. The higher your cost basis, the smaller your taxable gain. The smaller your taxable gain, the less you owe.

According to the IRS, capital improvements are permanent upgrades that add value, prolong the home's useful life, or adapt it to new uses — things like a new roof, kitchen remodel, HVAC system, added bathroom, finished basement, or installed solar panels. Routine repairs don't count. But major improvements very much do.

Here's the problem: the records homeowners most often lose are those for improvements. That's not a guess — it's what tax and legal experts consistently flag. And unlike business expenses, you don't report these improvements year by year. You need them years, sometimes decades, later — when you sell — and by then they're long gone from the kitchen drawer.

What Qualifies as a Capital Improvement — IRS Rules

- Additions: new room, bathroom, deck, garage, porch, patio

- Heating & cooling: new HVAC system, furnace, central air, ductwork

- Plumbing: new water heater, well, septic system

- Exterior: new roof, siding, windows, doors, gutters

- Interior: kitchen remodel, bathroom renovation, built-in appliances, flooring

- Landscaping: new lawn installation, irrigation system, fencing, driveway

- Systems: electrical rewiring, insulation, solar panels

Source: IRS Publication 523 — Selling Your Home; Rocket Mortgage

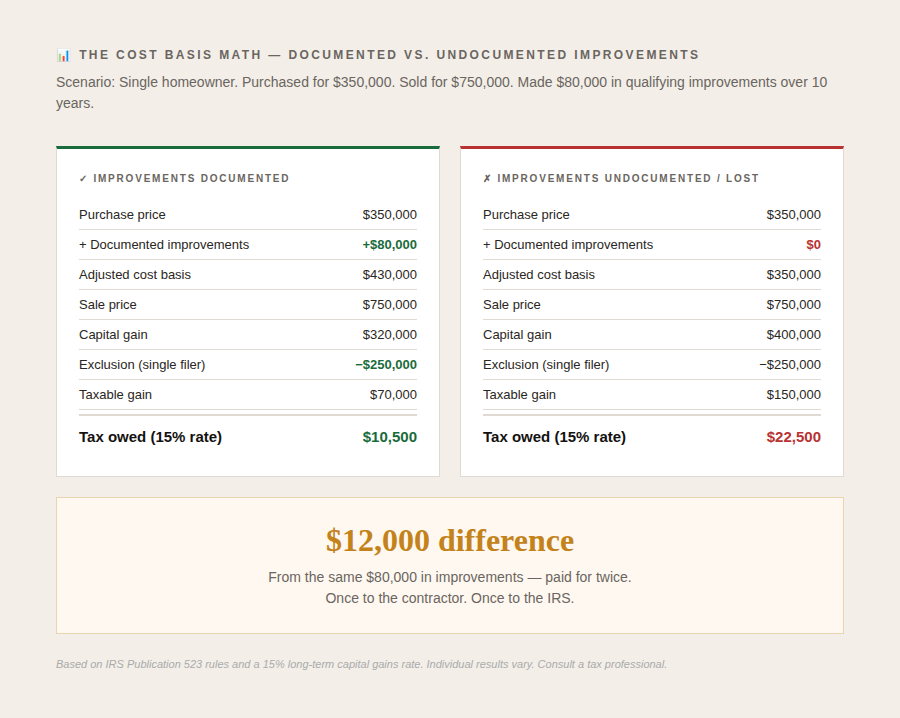

Scenario: Single homeowner. Bought for $350,000. Sold for $750,000. Made $80,000 in qualifying improvements over 10 years.

With Documentation:

- Purchase price: $350,000 + improvements: $80,000 = Cost basis: $430,000

- Capital gain: $320,000 — Exclusion: $250,000 = Taxable: $70,000

- Tax owed (15%): $10,500

Without Documentation:

- Purchase price: $350,000 + improvements: $0 = Cost basis: $350,000

- Capital gain: $400,000 — Exclusion: $250,000 = Taxable: $150,000

- Tax owed (15%): $22,500

Difference: $12,000 — from the same $80,000 in improvements. Paid for twice. Once to the contractor. Once to the IRS.

Based on IRS Publication 523 rules and a 15% long-term capital gains rate. Consult a tax professional for your situation.

The Scope of the Problem Is Bigger Than You Think

American homeowners are spending more on improvements than ever. According to the U.S. Census Bureau's American Housing Survey, homeowners spent approximately $827 billion on home improvement projects in the two-year period ending in 2023 — a 33% increase over the prior two-year period. The average project cost around $6,200. The most expensive projects — kitchen additions, full renovations — averaged close to $43,000 each.

That's an enormous amount of money. And the vast majority of it generates no paper trail that homeowners will actually be able to find in ten years. Contractors hand over invoices that get stuffed in a drawer. Permits are filed and forgotten. Receipts for materials fade or get tossed. When it's time to sell, homeowners are often left reconstructing years of spending from memory — which the IRS has no obligation to accept.

All of these qualify as capital improvements that increase your cost basis — if documented.

- Kitchen remodel / addition: ~$43,000 avg

- HVAC replacement: ~$17,700 avg

- Roof replacement: ~$15,000 avg

- Bathroom addition: ~$15,000 avg

- Typical project (all types): ~$6,200 avg

Sources: U.S. Census Bureau American Housing Survey 2023 (via NerdWallet); HIRI 2024; Empower Personal Dashboard data 2024

The math compounds over time

The average American homeowner lives in their home for 10 to 13 years before selling. In that time, they complete an average of 3.4 improvement projects annually. Even at modest per-project costs, that's tens of thousands of dollars in potential cost basis improvements — most of which will never be documented in a way that survives a decade in a junk drawer.

Now consider that home values roughly doubled over the past ten years. A homeowner who bought in 2015 for $350,000 may be sitting on a home worth $650,000 or more today. For a single filer, $300,000 in appreciation exceeds the exclusion by $50,000 — and every undocumented improvement makes that taxable overage larger.

How a $15,000 roof replacement goes from asset to liability in a decade.

- Year 1 — The Improvement: You replace the roof. $15,000. Contractor hands you an invoice. You put it "somewhere safe." (+$15,000 to your cost basis, if kept)

- Year 3 — The Move: You renovate or move. The invoice — in a folder with old cables and expired warranties — doesn't make the cut.

- Years 4–10 — The Forgetting: Life happens. More improvements made. Some documented, most not.

- Year 11 — The Sale: Your accountant asks for improvement documentation. You can't find it. Your cost basis is lower than it should be. ($2,250+ in avoidable taxes at 15% rate on $15,000)

What the IRS Actually Expects From You

The IRS doesn't come to you at closing with a demand. Instead, it's your responsibility — when filing the return for the year you sell — to calculate and document your adjusted cost basis. If you're audited, you need to be able to prove every improvement you're claiming: purchase orders, receipts, cancelled checks, bank statements, permits, contractor agreements.

Here's the part most homeowners don't know: you're required to keep these records for as long as you own the home — plus at least three to six years after you file the tax return for the year of sale. For a 10-year homeowner, that's potentially 16+ years of paperwork. Tax authorities and CPAs consistently note that improvement records are the single most commonly lost category of home documentation.

And if you can't prove an improvement? The IRS doesn't give you the benefit of the doubt. That improvement simply doesn't exist, and your cost basis stays lower.

What Documentation the IRS Wants to See

- Original receipts and invoices from contractors

- Purchase orders for materials

- Cancelled checks or bank/card statements showing payment

- Building permits (cities keep these — but you need them too)

- Before-and-after photos with date metadata

- Home inspection reports noting system updates

- Homeowner's insurance updates reflecting improvements

Sources: Nolo Legal Encyclopedia; R&A CPAs — Record Retention Guidelines

The Receipt Isn't Just About Taxes

The tax argument is the most quantifiable — but it's not the only reason documentation matters. An inspection report or home improvement record does three other jobs that most homeowners never think about until it's too late.

1. Insurance claims. If you've replaced your roof, added a deck, or installed new systems, your homeowner's insurance coverage should reflect it. When you file a claim, insurers ask for proof of what was there and what it cost. No documentation, no coverage — or coverage based on the old, lower value.

2. Buyer confidence. When you sell, buyers and their inspectors will ask what's been done. A documented history of improvements — with receipts, dates, and contractors — is a direct negotiating asset. Homes with verifiable improvement histories consistently attract stronger offers. It reduces uncertainty, which is what buyers pay a premium to avoid.

3. Warranty and contractor claims. Many contractors and product manufacturers offer 1-to-10 year warranties on systems and materials. Those warranties are tied to your receipt. No receipt, no claim — even if the issue surfaces well within the warranty window.

What To Do Starting Today

The good news: this is one of the most solvable financial problems a homeowner faces. It doesn't require a lawyer or an accountant. It requires a system — and the habit of using it.

- Save every contractor invoice and receipt digitally — a photo on your phone is acceptable to the IRS as long as it's legible and identical to the original

- Pull and keep copies of every building permit — your municipality keeps them, but you need your own copy too

- Take before-and-after photos with timestamps for every major project

- Log improvements in a running home record: date, contractor, cost, scope of work

- Upload your home inspection reports — they document system conditions at a point in time, creating a timeline the IRS and buyers can follow

- Update your homeowner's insurance after every major improvement and keep policy changes on file

- Keep all of the above for as long as you own the home, plus at least 3–6 years after you sell

Sources: SoFi; R&A CPAs; Nolo

If you've already lost some receipts, you're not necessarily out of options. Building permits are a matter of public record — most municipalities have them on file for decades. Bank and credit card statements can establish that a payment was made. Homeowner's insurance coverage increases and property tax assessment jumps can serve as third-party evidence. Contractors you've worked with may still have copies of old invoices.

But reconstruction is hard, stressful, and imprecise. The right time to build your documentation record is now — not in the year you list your house.

The receipt you threw away wasn't just a piece of paper. It was a claim on money you'd already earned — and without it, the IRS becomes a silent partner in your home's appreciation. Every improvement you made, every dollar you spent making your home better, is worth documenting. Not just for taxes. For insurance. For buyers. For the contractor dispute that might come three years from now.

Your home is almost certainly your largest financial asset. Treat its records the same way.

.png)